We’ve all been there. You’re scrolling through your phone after a long day or walking through your favorite store. Suddenly, something catches your eye. It could be a stylish tech accessory, a simple kitchen gadget, or a piece of clothing that promises to refresh your wardrobe. It feels harmless, costing only $25 [approx. ₹2,400]. You justify the purchase right away. “It’s under thirty bucks,” or “I’ve worked hard this week; I deserve a little treat.” You add it to your cart, make the payment, and enjoy that quick rush of happiness.

But what happens a week later if you examine your habits? The excitement fades. That item now sits quietly in a corner, collecting dust and contributing to the mess in your home. More importantly, your bank account is now $25 [approx. ₹2,400] further from your emergency fund goals, investment targets, or long-term financial freedom.

Impulse buying is rarely a math problem; it’s almost always rooted in emotions. Traditional budgeting tells you to cut back, track every penny, and rely on pure willpower. But willpower runs out. When you’re tired, stressed, or bored, willpower gives in. To truly manage impulse spending, you don’t need a stricter budget. You just need to create a system of mindful rules.

Enter the “One-In, One-Out” Rule.

What is the “One-In, One-Out” Rule?

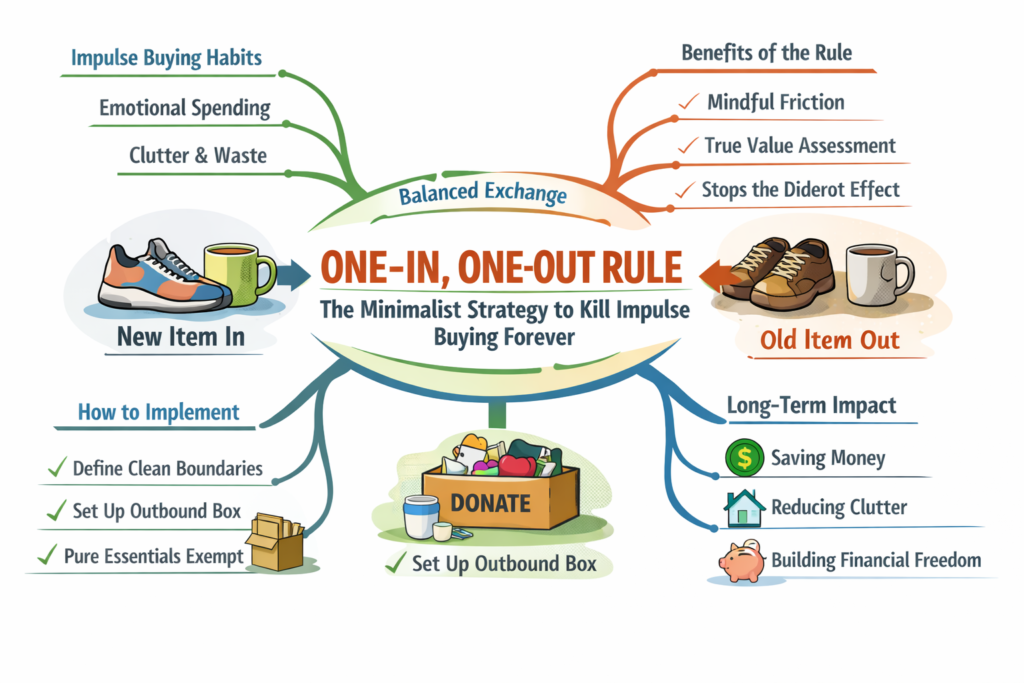

The idea is simple yet challenges our modern shopping habits: Before you bring any new non-essential item into your life, you must let go of an existing item.

If you want to buy a new pair of casual sneakers for $60 [approx. ₹5,760], you must find an old pair of shoes to donate, sell, or recycle. If you want a new ceramic coffee mug for $15 [approx. ₹1,440], an old mug in your kitchen must go. If you want to upgrade to a newer tablet case for $40 [approx. ₹3,840], your current case has to be removed and dealt with responsibly.

By tying each new purchase to a direct consequence in your living space, you change how you think about your money and environment. You aren’t just swapping digital numbers in a bank; you’re trading your space and peace.

The Psychology of the Rule: Why It Protects Your Financial Stability

This strategy isn’t just a quirky way to declutter; it serves as a smart psychological tool that shields your finances. Here are three main reasons why this rule protects your money:

- It Restores Mindful Friction to Modern Shopping

The modern retail world is designed to make buying easy. One-click ordering, saved card details, facial recognition payments, and instant digital wallets make purchases almost effortless. Your brain doesn’t even have time to register the loss of your money before the sale is marked “Successful.”

The “One-In, One-Out” rule acts as a necessary speed bump. Before you hit “buy” or hand over your card for a $100 [approx. ₹9,600] jacket, you need to pause. You physically walk to your closet, look through your things, and decide what you are willing to give up. This pause disrupts the impulse and allows your logical side to regain control.

- It Forces a Real Measure of True Value

When you’re in the heat of the moment, you focus only on the good aspects of the new item. You notice its nice condition, marketing claims, and the lifestyle it promises.

But with this rule, you have to compare the new item to something you already own and value. You start asking important questions: “Is this new water bottle for $35 [approx. ₹3,360] really better than my insulated flask that has kept my drinks cold for two years?” “Am I really willing to donate a shirt that fits me perfectly to make space for a trendy new one?”

If you find you aren’t willing to part with your current items, the illusion of “need” disappears. The impulse fades, and your money stays safe in your savings account.

- It Stops the Destructive “Diderot Effect”

Named after the French philosopher Denis Diderot, this phenomenon shows how buying one new item can trigger a cycle of further unnecessary purchases. For example, if you spend $150 [approx. ₹14,400] on a new desk, you might feel compelled to buy a new chair for $200 [approx. ₹19,200] because the chair now looks out of place. Then you might buy a new $30 [approx. ₹2,880] lamp because the old one seems outdated.

The “One-In, One-Out” rule puts a strict limit on this cycle. By refusing to allow your space to grow, you also limit your additional spending. It stops the chain reaction before it sets in.

How to Implement the Rule This Week: A 3-Step Practical Guide

If you want to shift your life and finances toward intentional minimalism, it doesn’t have to be stressful. You can easily adopt this rule by following these three steps:

- Define Clean Boundaries:

Keep exchanges within the same product family. A new book replaces an old book; a new beauty product replaces an old one; a new tech tool replaces an old piece. Don’t try to game the system by trading a cheap pair of socks for a luxury television. Keep the exchanges fair. - Establish a Dedicated Outbound Box:

Designate a specific box in your closet or storage area as your official “Outbound Station.” The moment you bring in a new non-essential item, the item it replaces must go right into that box. No exceptions or delays. Once the box is full, take it to a local donation center or sell the items online to get some cash back. - Grant Complete Amnesty to Pure Essentials:

Be clear about the difference between everyday needs and lifestyle wants. This strategy aims to limit excess consumerism, not to restrict necessary living. You shouldn’t throw away an old toothbrush to buy a new one, and you don’t need to discard a good pot just because your frying pan broke. Protect your essentials while holding lifestyle wants to a high standard.

The Long-Term Financial Impact

Let’s look at the numbers over time. If the “One-In, One-Out” rule helps you avoid just two minor $50 [approx. ₹4,800] impulse purchases each month, you’ll save an extra $100 [approx. ₹9,600] monthly.

Over a year, that adds up to $1,200 [approx. ₹1,15,200] safely in your pockets. If you invest that saved money in a low-cost index fund or build your six-month emergency fund, you’re using small, daily mindful choices to build long-term wealth.

The Minimalist Mindset: Financial minimalism isn’t about punishing yourself or living in deprivation. It’s about clearing out consumer noise so you can appreciate and make the best use of what you already own.

Next time you feel tempted to click “Buy Now” or approach a checkout counter, take a deep breath. Pause and ask yourself, “What am I really willing to let go of to make room for this?”

If nothing comes to mind, close the tab or put the item back. You haven’t missed anything—instead, you’ve achieved a victory for your home, clarity, and financial freedom.

What do you think? Could the “One-In, One-Out” rule help you get control over impulse spending? What category—like clothes, shoes, gadgets, or books—do you struggle with clutter and impulse purchases? Let’s chat in the comments!